Content provided by WalletHub.

A lot of people probably assume that giving credit cards to college kids is a recipe for trouble, and many students are no doubt among them. But if you ask a diverse sample of college students about their understanding and usage of credit cards, as WalletHub did, the results may just surprise you – in a good, reassuring way.

WalletHub conducted a nationally representative survey of college students, asking about everything from how they’d grade their financial know-how to which spending categories they most want bonus credit card rewards for. You can check out the results in the following infographic.

Money-Saving Tips For College Students

Identifying the best student credit card is only half the battle. You also need to use it responsibly, avoid common money-management mistakes, and build financial literacy for success after graduation.

- Consider Credit Building Your Top Priority – A good credit score will save you thousands of dollars per year on loans, lines of credit and insurance premiums. It may even help you land your dream job or lease a new car. And two of the keys to building a good credit score are making on-time payments and establishing a long track record of responsible borrowing.

- Don’t Make Purchases If You Don’t Trust Yourself – Credit cards report information to the major credit bureaus every month even when you don’t make any purchases. And while you may build credit faster by making purchases and paying them off by the end of the month, overspending and missing payments is counterproductive.

So if you don’t trust yourself to spend responsibly with plastic, give your card to your parents for safekeeping. You could even cut it up. Just make sure to save your account number in case you need to call customer service. - Make a Budget – If you combine credit card use with a well-defined budget while in college, you’ll be well ahead of the curve. Only two in five consumers have a budget, according to the National Foundation for Credit Counseling, and that’s one of the main reasons why credit card debt levels are so high.

To learn how to take this important step, check out WalletHub’s step-by-step guide on how to make a great budget. - Take Advantage of Campus Resources – Most colleges and universities offer financial literacy resources of some sort. For example, there might be a personal finance class you can take, a money-management help center you can visit or online educational materials to peruse. Find out and soak up as much information as you can, especially if it will fulfill a curriculum requirement. Because unlike much of what you’ll learn in college, financial skills translate directly to everyday life.

- Approach Student Loans with Caution – Taking out a bunch of student loans might not seem like a big deal now, considering how long you’ll have to pay them off. But too few students truly consider how big of a burden they can wind up being. Student debt increases the pressure to find a job and can delay major life events such as buying a home, getting married or starting a family.

No one wants to be paying off education debt into their 40s, which is all too common these days. So try to supplement your tuition money with scholarships, grants and work experience. This will also give your resume a boost. - Improve Your Financial Literacy – Understanding how to manage money is an invaluable life skill. And you probably won’t learn much about in school. So you’ll have to take things into your own hands. To get a sense of your current knowledge level and the areas where you can improve the most, get your WalletLiteracy Score.

How to Pick the Best Student Credit Card for You

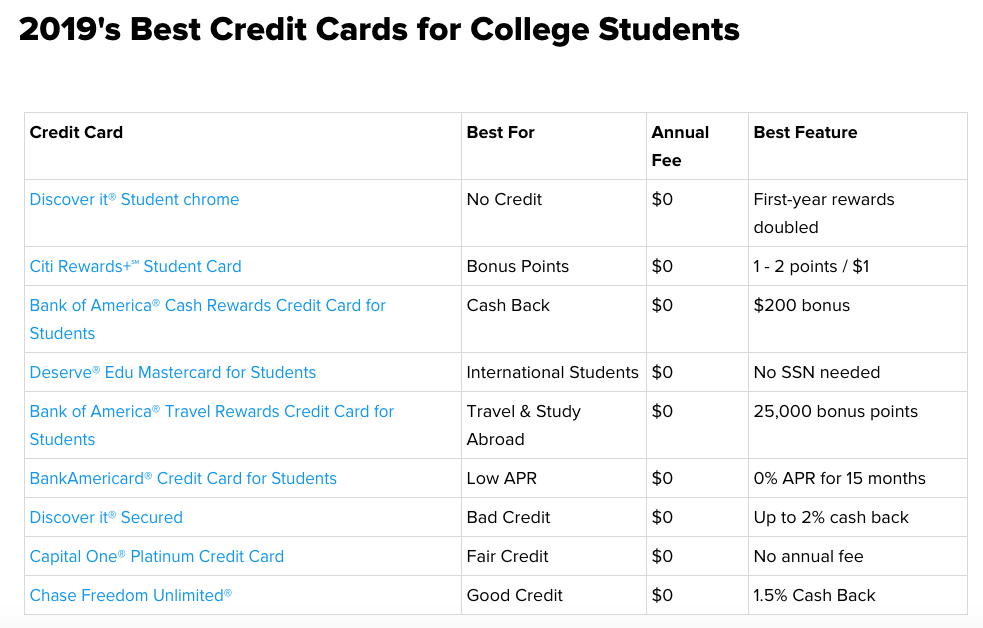

The best credit card for college students is Discover it® Student chrome because it has a $0 annual fee, gives 1 – 2% Cash Back on purchases, and doubles all the rewards cardholders earn the first year. The Discover it® Student chrome card also offers an introductory APR of 0% for 6 months on new purchases (14.99% – 23.99% (V) APR after) and has a $0 foreign transaction fee. So it’s a great all-around offer, no matter where your studies take you.

But there are plenty of other contenders, some of which may turn out to be better for you, depending on your exact needs. For example, the best credit card for college students who want to travel is the Bank of America® Travel Rewards Credit Card for Students, which offers an initial bonus of 25,000 points and much more. And the best student credit card for low interest rates is the BankAmericard® Credit Card for Students, which gives 0% for 15 months on purchases and balance transfers, with a $0 annual fee and a $0 balance transfer fee.

But even though WalletHub’s editors have done the work to highlight the best student credit cards on the market, you still have to decide which offer is right for your particular needs. And these rules of thumb will help you pinpoint that plastic.

How to find the best student credit card for your needs:

- Rule Out Cards with Annual Fees. Students should always limit their search to cards that don’t charge annual fees. A student’s top priority for using a credit card is to build credit, after all, and most college students have limited budgets. So the best student credit cards are therefore those that are basically free to maintain.

- Focus on Rewards if You Plan to Pay in Full. Paying your bill in full every month is the best approach because it will save you from expensive interest charges and help you avoid getting into the bad habit of spending above your means. And since interest rates don’t matter when you pay in full, you can concentrate on getting the most lucrative rewards for your spending habits.

- Find a 0% Rate for Big-Ticket Purchases. There are a handful of 0% APR student credit cards available, any of which could save you a boatload if you plan things right. That means applying a few weeks before your desired purchase date and repaying your balance before regular rates take effect. WalletHub’s Credit Card Payoff Calculator can help with that.

- Transfer a Balance If You’re in Credit Card Debt. A few student credit cards offer 0% intro rates on balance transfers. With that being said, you’ll need to consider more than just the length of the 0% term, including each card’s balance-transfer fee and regular APR. You can crunch the numbers with WalletHub’s Balance Transfer Calculator to see which offer would save you the most money.

- Get a Secured Card If You’re Rejected. Secured cards are the easiest type of credit card to get approved for. The reason is this: They require a refundable security deposit that serves as the account’s spending limit and reduces risk from both the student’s and issuer’s perspective. They also are indistinguishable from unsecured credit cards on your credit reports, which means you can build credit and practice responsible habits without running the risk of exacerbating your situation. So, if you have damaged credit, opening a secured card and rebuilding your credit standing is a must.

- Consider Applying with a Cosigner. Very few credit card companies these days allow people to apply for a credit card with a co-signer. But if you find an eligible offer, a co-signer with better credit than you could help you qualify for a better card than you’d get on your own. Similarly, becoming an authorized user on a parent’s credit card account is an easy way to start, or continue, the credit-building process.

Methodology: Picking the Best Student Credit Cards

To identify the best credit cards for college students, WalletHub’s editors compare 1,000+ credit card offers based on their approval requirements, rewards, rates and fees. We focus on student-branded credit cards with $0 annual fees because they tend to be the best deals and are relatively easy for college students with limited-to-no credit history to get.

Keeping costs down and establishing responsible habits are key for college students. So we generally recommend getting a credit card with great rewards and paying the bill in full every month. However, our best-card picks typically include options with low interest rates, too.

Although credit card companies typically offer the best limited-credit deals to students, WalletHub’s editors also consider general-purpose credit cards for which some students may be eligible. For example, students who have already made mistakes with credit or are concerned about overspending may want to consider a secured credit card. And students who already have good credit as a result of being an authorized user on a parent’s account may want a higher-level card.